By: Felicity Bradstock View the original article here

There is great optimism around the future of green hydrogen, with many seeing it as a super-fuel that will replace oil-derived options, as well as be highly competitive with electric battery technology. However, we are far from achieving this ambition yet, mainly due to small-scale production operations and high costs. Many companies around the globe have plans to produce green hydrogen, but some are battling challenges that are slowing down the rollout of the clean fuel. Despite improvements in production processes, thanks to greater investment in the sector in recent years, the production and transportation costs of green hydrogen remain much higher than other fuels, including other types of hydrogen.

Producing grey or blue hydrogen, which is derived from fossil fuels, is viewed as relatively low cost, with many companies already relying on this fuel. Grey hydrogen is produced using natural gas. It undergoes a steam methane reforming (SMR) process, which breaks methane apart using high-pressure steam, which creates separate hydrogen, carbon monoxide, and carbon dioxide molecules. This process produces high levels of carbon dioxide, around 9 to 10 tons of CO2 for every ton of hydrogen. But it is also highly cost-effective, so long as natural gas prices remain stable. In July 2022, the cost of grey hydrogen was around $2 per kilo.

In contrast, green hydrogen production methods are more expensive. Green hydrogen is made using renewable energy sources to power an electrolysis process that separates hydrogen from water, producing just steam as a waste product. It is carbon neutral, making it highly attractive for companies looking to decarbonize. However, by July 2022, it cost around $4 to $5 a kilo, or even more, to produce green hydrogen. And some industry experts believe that the high cost of green hydrogen production isn’t going to fall any time soon.

Green hydrogen is viewed by many international agencies, such as the International Energy Agency (IEA) and the International Renewable Energy Agency (IRENA), as a solution to decarbonize ‘hard-to-abate’ sectors. As more governments and private companies around the globe pump funding into green hydrogen operations, there are high hopes that the production cost of green hydrogen to fall substantially, to as low as $0.5 per kilo. However, others believe it will be difficult to drive the cost to lower than $3 per kilo.

IRENA published two studies to drive green hydrogen production worldwide: Green Hydrogen: A Guide to Policy Making in November 2020, and Green Hydrogen Cost Reduction: Scaling up Electrolysers to Meet the 1.5°C climate goal in December 2020. These studies were aimed at encouraging governments and private companies to scale up production, aimed at driving down costs. However, the price of green hydrogen production so far remains elevated, at around 2 to 3 times the cost of grey hydrogen production, when gas prices are stable.

Nevertheless, progress has been seen thanks to greater funding into research and development, with the price of electrolysers falling by around 60 percent since 2010. According to IRENA, they could decrease by a further 40 percent in the short term and by as much as 80 percent in the long term. This cost reduction prediction relies on greater innovation in electrolysis technology to improve its performance, as well as scaling up manufacturing capacity, standardization, and growing economies of scale.

Another challenge to consider is the cost of transportation. Murray Douglas, the head of hydrogen research at Wood Mackenzie, stated that “Hydrogen is pretty expensive to move… “It’s more difficult to move than natural gas … technically, engineering wise … it’s just harder.” And Douglas is not the only one concerned about this. The U.S. Department of Energy (DoE) has reported challenges with green hydrogen including “reducing cost, increasing energy efficiency, maintaining hydrogen purity, and minimizing hydrogen leakage.” The DoE believes greater research is required to “analyze the trade-offs between the hydrogen production options and the hydrogen delivery options when considered together as a system.”

Companies worldwide are now considering the best locations for their green hydrogen production facilities. While there is great potential for the development of plants in Australia, North Africa, and the Middle East, these could be very far from their principal markets. Douglas highlighted the need for a dedicated pipeline, constructed between the producer and end-user if moving green hydrogen by pipe. Alternatively, green hydrogen could be transported as ammonia with nitrogen, which could be shipped and sold to consumers such as fertiliser producers. Otherwise, users would have to crack the ammonia back into nitrogen, which would increase costs and result in energy losses.

For green hydrogen to be as successful as everyone hopes, it will require significant investment to overcome these challenges. Jorgo Chatzimarkakis, the CEO of the industry association Hydrogen Europe, suggests the need for a certification system, to guarantee that any green hydrogen production was powered by renewable sources. Further, a well-researched delivery strategy needs to be developed to ensure that production facilities are adequately linked with green hydrogen markets. This has been seen in projects such as Cepsa’s green hydrogen corridor between southern and northern Europe.

While transportation costs are high, companies already understand how to move green hydrogen as they have been doing it the same way with natural gas for decades. But some are deterred by high costs. Therefore, the industry must drive down production costs to alleviate some of the pressure on transportation. Although the green hydrogen industry continues to face several major challenges, preventing a wide-scale deployment of the clean fuel, greater investment in the sector over the coming decades will likely fix many of these problems and allow for the deployment of global, large-scale green hydrogen production.

The global need for grid-scale energy storage will rise rapidly in the coming years as the transition away from fossil fuels accelerates. Energy storage can help meet the need for reliability and resilience on the grid, but lithium-ion is not the only option, writes Oliver Warren of climate and ESG-focused investment bank and advisory group DAI Magister.

Dubbed the “decade of delivery” by the World Economic Forum (WEF) and the ‘Decade of Action’ by the International Renewable Energy Agency, the 2020s is a crucial decade for the energy transition. However, to realise the full potential of renewables and meet ambitious energy transition objectives, we must have the capacity to store energy more effectively.

Many stakeholders are pinning their long-term storage hopes on lithium-ion (Li-ion) battery storage solutions, with this market expected to grow by almost 20% per year between 2022 and 2023, according to Precedence Research.

But the reality is that, although Li-ion batteries have an important role to play on the road to net zero, this technology is neither robust nor versatile enough to single-handedly fulfil energy storage requirements.

As a result, a diverse range of alternative grid-scale solutions that can deliver an unprecedented expansion in storage capacity are needed to offset our reliance on Li-ion batteries and drive the renewable energy transition.

Ramping up capacity

According to the International Energy Agency (IEA), to decarbonize electricity globally the world’s energy storage capacity must increase by a factor of 40x+ by 2030, reaching a total of 700 GW, or around 25% ofglobal electricity usage (23,000TWh per annum). For comparison, this would be like swelling the size of the UK’s land to that of the USA.

Similar to how “nobody ever gets fired for buying IBM”, lithium-ion holds a similar place in grid scale electrical storage today. With the 2020s being the decade of energy storage, investors need to focus on alternative storage solutions which may require higher capex up front, but deliver lower long term levelized cost of electricity and longer asset lifetime.

Li-ion batteries, long touted as a vital technology for grid-scale storage, are neither feasible nor sustainable. Cobalt extraction, a fundamental component of Li-ion batteries, is highly toxic and polluting. Limited cobalt supply is a major issue, especially considering the rapidly growing demand for electric car batteries and backup generators. Relying solely on Li-ion technology also leaves us vulnerable to a single supply chain and the availability of access to critical elements e.g., cobalt, in some of the most volatile regions of the world, such as the Democratic Republic of the Congo (DRC).

That isn’t to imply that Li-ion batteries don’t have their place, but they should target fast frequency response rather than load following. Li-ion batteries are best suited to replace gas-fired peaking plants e.g., open cycle gas turbines (OCGTs) and supplement pumped hydro during evening peaks. However, they lack the capacity and duration (more than a few hours of drawdown) to load follow, unlike combined cycle gas turbines (CCGTs), throughout the course of a day.

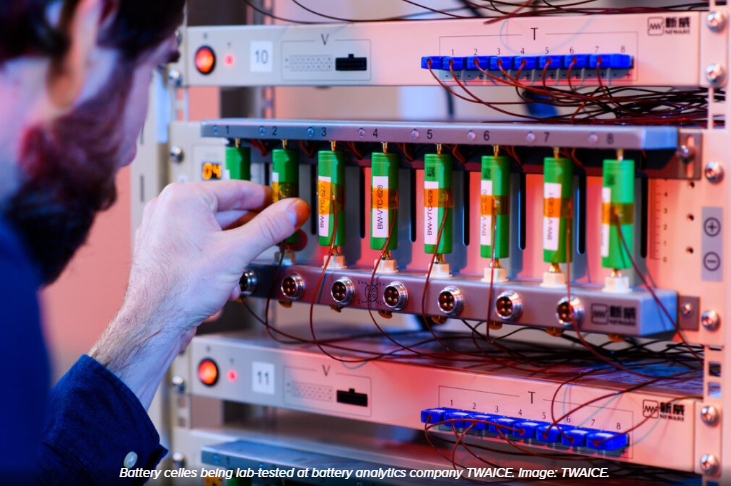

They are also prone to damage from failing to complete full discharge and recharge cycles although battery analytics companies such as PowerUp and Twaice are trying to solve this problem.

In addition, Li-ion batteries have limited lifespans of up to 10 years before needing replacement. All these factors make Li-ion batteries unviable at grid scale and necessitate the use of alternatives.

Vehicle-to-grid (V2G) technology, which will enable the aggregation of part of the storage capacity of the more than 140 million electric vehicles expected globally by 2030, could bring more than 7TWh in Li-Ion-based additional energy storage that can be drawn from at a moment’s notice, but faces the similar limitations as grid based Lithium Ion batteries.

Viable grid-scale storage alternatives

No single killer application or technology exists to get the job done. Diversification is key with success dependent on the wide-scale adoption of multiple grid-scale energy storage solutions:

Compressed air/gas storage

New compressed air and gas storage technologies offer a novel way of storing energy as compressed air or gas. They can store more energy in a smaller space and for more extended periods than other forms of energy storage like batteries.

Italian start-up Energy Dome has found an unexpected way to store green energy. The company’s ground-breaking long-duration energy storage system compresses CO2 into a liquid and stores it in a massive, pressurised dome. CO₂ has a higher density than air which results in denser energy storage and doesn’t need advanced materials and expensive insulation compared to liquid air at cryogenic temperatures.

Augwind Energy is an Israeli technology company revolutionizing energy storage at scale by storing compressed air underground in large tanks made from unique polymers. The company’s AirBattery solution uses only air and water to store energy safely and cost-effectively at high capacity for long durations.

The solution uses an external energy source, be it from the grid or renewable sources to power water pumps. AirBattery can run endless cycles for decades with no degradation and at a minimal cost.

Cheesecake Energy is a UK-based spinout company founded on thermal and mechanical energy storage research undertaken at the University of Nottingham. The company has developed eTanker, a new energy storage system that stores electricity as heat and compressed air. Electric motors operate compressors that store air and heat at high pressure in storage units to store energy. To produce electricity, the same compressors act as expanders, which turn a generator.

The eTanker is a long-lasting (20+ years) and environmentally friendly energy storage solution built from recyclable raw materials. It can deploy across a variety of static applications such as industry, agriculture, transport, and renewable generation, replacing the need for lithium-ion batteries.

Highview Power also hails from the United Kingdom. The company has developed a large-scale energy storage system for utility and distribution power networks. Highview’s low-cost liquid-air energy storage solution uses the process of cryogenic cooling to store energy for future use.

The system gathers energy from renewable sources like wind and solar and stores it in tanks as liquid air at low temperatures. Liquid air gets heated when required, causing the stored energy to release as a gas. This gas is then used to generate electricity by powering turbines.

Highview plans to raise £400 million (US$483.5 million) to build the world’s first commercial-scale liquid air energy storage (LAES) plant to boost renewable power generation in the UK. Of the £400 million, the company intends to spend £250 million to construct a 30MW storage plant that can store 300MWh of electricity. The remaining £150 million would go towards engineering for a further four sites. Highview already has a 5MW pilot plant in operation in England.

Innovative pumped hydro

Innovative pumped hydro energy storage (PHES) uses renewable energy to pump water from a lower reservoir to an upper reservoir. During periods of high demand, the water releases from the upper reservoir to generate electricity. This type of energy storage is more efficient and cost-effective than traditional pumped hydro and requires less land.

Ocean Grazer, a Dutch start-up, has come up with a unique offshore energy storage system that can deploy at the source of power generation. The Ocean Battery is a pumped hydro system that stores energy from offshore wind farms by pumping water back and forth into flexible bladders where it is stored at different pressures. When there is a demand for power, water rushes back from the bladders to the reservoirs driving multiple hydro turbines to generate electricity.

The Ocean Battery is significantly less expensive to build than existing large-scale lithium-ion battery systems, which require massive platforms made from sea containers. Furthermore, the Ocean Battery has a far longer lifespan, lasting up to one million charging cycles, compared to the 5,000-10,000 offered by lithium-ion batteries.

RheEnergise has developed a ‘High-Density Hydro’ system that stores and releases electricity from hills rather than mountains or dam walls. In contrast to other systems, it uses a non-toxic, high-density additive for its closed-loop pumped storage. This allows it to create 2.5x the energy of traditional pumped storage systems while also having reduced environmental impacts and lower costs.

The High-Density Hydro system has the potential to enable hillsides across the UK to store energy for the country’s electricity supply, considerably expanding the range and output of pumped storage. The company expects to have its first commercial system operational by 2024.

Thermal energy storage

Thermal energy storage works by storing thermal energy as heat, usually in a material such as water, rock, or soil. Heat gets stored in various ways, including using phase-change materials, which absorb and release heat at specific temperatures. The stored heat can then generate electricity. Thermal energy storage can store excess energy from solar, wind, or other renewable sources during peak energy demand hours or when the renewable source is unavailable

Lumenion is a renewable energy storage technology company that provides large-scale energy storage solutions. The company’s TESCORE solution is a high-temperature storage system that stores fluctuating wind and solar PV power as thermal energy with virtually loss-free conversion.

Japanese companies Toshiba, Marubeni and Chubu Electric Power have collaborated with the support of the Japanese Ministry of the Environment to develop a pilot rock-based thermal energy storage system that’s more environmentally friendly and efficient than lithium-ion batteries and hydrogen.

The system has a capacity of 100kWh and can use storage materials such as crushed stone, bricks, molten salt, and concrete. Thus far, it’s claimed that the system can store heat at temperatures above 700°C with a small heat storage tank.

Over the next few years, the goal is to build a larger facility with 500kWh capacity and launch commercial projects based on rock heat storage technology.

Gravity storage

Gravity storage is a form of energy storage that utilizes the force of gravity to store and release potential energy. It works by raising weights, typically made of concrete, bricks, or rocks, and then releasing them to generate electricity when needed.

Energy Vault, based out of Switzerland, is a market leader in gravity storage. The company’s breakthrough technology was inspired by pumped hydro plants that rely on the power of gravity and movement of water to store and discharge electricity.

Their solution employs a proprietary mechanical process and energy management system to store and dispatch electricity. When renewable energy generation is high, the solution harnesses that energy to lift 30-tonne bricks to an elevated height with potential energy stored in the bricks. The system releases kinetic energy back to the grid through the controlled lowering of the bricks under gravitational force to generate electricity.

The management system orchestrates the energy charge/discharge while accounting for various factors, including energy supply and demand volatility, weather elements and other variables.

Storage is a fundamental enabler of the energy transition

Our ability to expand energy storage capacity is one of the most pressing issues that will determine whether this defining ‘transitional’ decade is a success. But we’ll need to invest wisely into the right technologies that get the greatest bang for the buck (in terms of GWh capacity and return on capital) given the limited lifespan of Li-Ion and the decarbonization of the grid.

At a current capital cost of US$2,000 per kW quoted by the US National Renewable Energy Laboratory (NREL) for 6-hour Li-ion battery storage, the 700GW of capacity needed by 2030 equates to around a US$1.5 trillion market over the coming decade, making it worth nearly US$200 billion a year.

Annual investment worldwide into promising energy storage companies is currently running at only US$9 billion in 2022 according to Pitchbook. As the crucial nature of this market becomes more and more clear to investors, there needs to be an exponential increase in investment. Within energy transition, the market for energy storage offers one of the largest ‘blue-ocean’ opportunities for investors available anywhere in the world today.

By: Casey Crownhart View the original article here

Buckle up, because this week, we’re talking about batteries.

Over the past couple of months, I’ve been noticing a lot of announcements about a new type of battery, one that could majorly shake things up if all the promises I’m hearing turn out to be true.

The new challenger? Sodium-ion batteries, which swap sodium for the lithium that powers most EVs and devices like cell phones and laptops today.

Sodium-ion batteries could squeeze their way into some corners of the battery market as soon as the end of this year, and they could be huge in cutting costs for EVs. I wrote a story about all the recent announcements, and you should give it a read if you’re curious about what companies are jumping in on this trend and what their plans are. But for the newsletter this week, let’s dig a little bit deeper into the chemistry and consider what the details could mean for the future of EV batteries.

Top dog

One of the reasons that lithium dominates batteries today is absolutely, maddeningly simple: it’s small.

I mean that in the most literal, atomic sense. Lithium is the third-lightest element, heavier than only hydrogen and helium. When it comes down to it, it’s hard to beat the lightest metal in existence if you’re trying to make compact, lightweight batteries.

And cutting weight and size is the goal for making everything from iPhones to EVs: a lightweight, powerful battery means your phone can be smaller and your car can drive farther. So one of the primary ways we’ve measured progress for batteries is energy density—how much energy a battery can pack into a given size.

When you look at that chemical reality, it’s almost no wonder that lithium-ion batteries have exploded in popularity since their commercial debut in the 1990s. There are obviously other factors too, like lithium-ion’s ability to reach high voltages in order to deliver a lot of power, but the benefit of being lightweight and portable is hard to overstate.

Lithium-ion batteries have also benefited from being the incumbent. There are countless researchers scouring the world for new materials and new ways to build lithium-ion cells, and plenty of companies making them in greater numbers—all of which adds up to greater efficiencies. As a result, costs have come down basically every year for decades (with the notable exception of 2022).

And at the same time, energy density is ticking up, a trend I’m personally grateful for because I often forget to charge my phone for days at a time, and it typically works out much better when that happens now than it did a few years ago.

Branching out

But just because lithium-ion dominates the battery world today doesn’t mean it’ll squash the competition forever.

I’ve written about the growing number of options in the battery industry before, mostly in the context of stationary storage on the electrical grid. This is especially important in the transition to intermittent renewable energy sources like wind and solar.

While backup systems tend to use lithium-ion batteries today since they’re what’s available, many companies are working to build batteries that could eventually be even cheaper and more robust. In other words, many researchers and companies want to design batteries specifically for stationary storage.

New batteries could be made with abundant materials like iron or plastic, for example, and they might use water instead of organic solvents to shuttle charge around, addressing lingering concerns about the safety of large-scale lithium-ion battery installations.

But compared to stationary storage, there are fewer candidates that could work in EV batteries, because of the steep demands we have for our vehicles. Today, most of the competition in the commercial market is between the different flavors of lithium-ion batteries, with some lower-cost versions that don’t contain cobalt and nickel gaining ground in the last couple of years.

That could change soon too, though, because just below lithium on the periodic table, a challenger lurks: sodium. Sodium is similar to lithium in some ways, and cells made with the material can reach similar voltages to lithium-ion cells (meaning the chemical reactions that power the battery will be nearly as powerful).

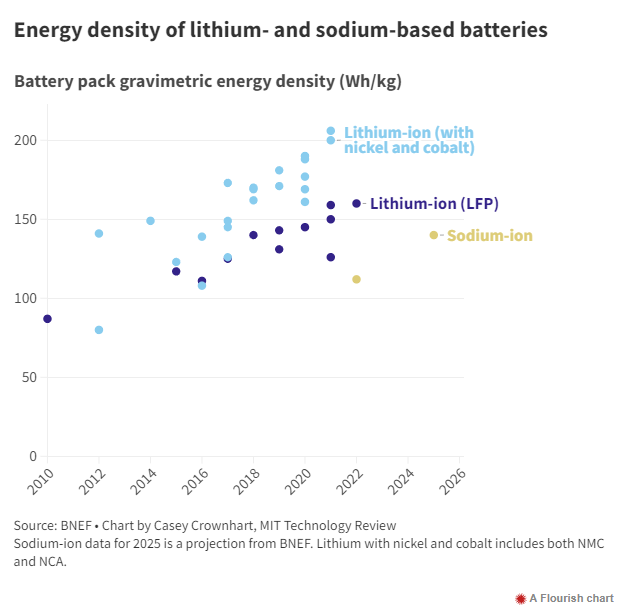

And crucially, sodium-based batteries have recently been cramming more energy into a smaller package. In 2022, the energy density of sodium-ion batteries was right around where some lower-end lithium-ion batteries were a decade ago—when early commercial EVs like the Tesla Roadster had already hit the road.

Projections from BNEF suggest that sodium-ion batteries could reach pack densities of nearly 150 watt-hours per kilogram by 2025. And some battery giants and automakers in China think the technology is already good enough for prime time. For more on those announcements and when we might see the first sodium-battery-powered cars on the road, check out my story on the technology.

Related reading

Here’s how sodium batteries could get their start in EVs.

I wrote about the potential for this sort of progress in a story from January about what we might see forbatteries this year.

Sodium could be competing with low-cost lithium-ion batteries—these lithium iron phosphate batteries figure into a growing fraction of EV sales.

Take a tour of some other non-lithium-based batteries:

Iron-based batteries could be a cheap way to store energy on the grid and assuage concerns about safety.

What about using plastic instead?

Some companies want to go beyond batteries entirely to store energy.

Another thing

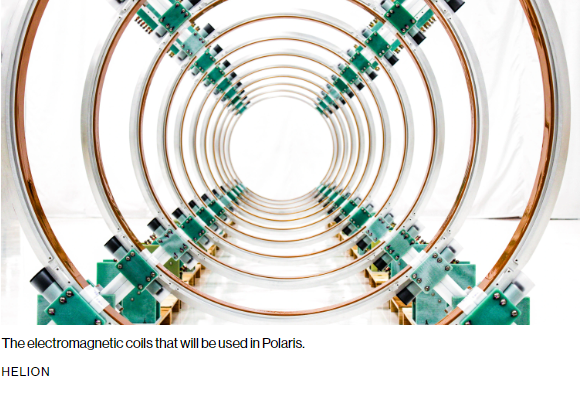

A startup says it’ll be ready to turn on the world’s first fusion power plant in five years. Yes, you read that right: five years.

Helion Energy, a fusion startup backed by OpenAI’s Sam Altman, announced that it’s lined up an agreement to sell electricity to Microsoft. The company says its first plant will come online in 2028 and will reach full capacity (50 megawatts of output) within a year after that.

As you might remember, the energy world reached a huge milestone in December when a fusion reaction generated more energy than what was put in to start it. But for a lot of reasons, that symbolic moment doesn’t necessarily mean cheap fusion power is within our grasp. And some experts are pretty skeptical about Helion’s announcement. Read more about the details in this story from my colleague James Temple.

Keeping up with climate

Need a few extra miles of range on your EV? Might as well slap some solar panels on the roof. But don’t expect too much of a boost. (Bloomberg)

For the first time in my entire life, I seem to be experiencing seasonal allergies. And climate change might have something to do with it. (The Atlantic)

Companies might be overselling the potential for so-called “renewable natural gas.” While it can cut emissions relative to fossil sources, critics worry that putting too much stock in methane made from cow manure or food scraps will slow efforts to ditch fossil fuels. (Canary Media)

→ I wrote earlier this year about how the process to make and capture methane from food scraps works. (MIT Technology Review)

Aubrey Plaza is hilarious and a gift to this world, but some people aren’t so happy about a recent ad she did for the dairy industry that takes aim at plant-based milks. (Vox)

India might stop adding new coal power plants to the pipeline. While this wouldn’t stop all current construction, it could be a major boost to the country’s emissions cuts. (Reuters)

A lot of the work to improve battery performance has been basically focused on one half of the device: the cathode. But some companies are working hard to improve the often-overlooked anodes by using silicon. (IEEE Spectrum)

→ Silicon anodes from startup Sila made their debut in fitness trackers nearly two years ago. The next stop? EVs. (MIT Technology Review)

Support for nuclear power in the US just reached its highest level in over a decade, according to a new Gallup poll. (Grist)

Electric vehicles made up 80% of Norway’s new car sales last year. The country provides a picture of the potential future for electrified transport’s benefits (cleaner air!) and challenges (long charging lines). (New York Times)

By: Catherine Clifford View the original article here

Service technicians work to install the foundation for a transmission tower at the CenterPoint Energy power plant on June 10, 2022 in Houston, Texas. Brandon Bell | Getty Images News | Getty Images

Building new transmission lines in the United States is like herding cats. Unless that process can be fundamentally improved, the nation will have a hard time meeting its climate goals.

The transmission system in the U.S. is old, doesn’t go where an energy grid powered by clean energy sources needs to go, and isn’t being built fast enough to meet projected demand increases.

Building new transmission lines in the U.S. takes so long — if they are built at all — that electrical transmission has become a roadblock for deploying clean energy.

“Right now, over 1,000 gigawatts worth of potential clean energy projects are waiting for approval — about the current size of the entire U.S. grid — and the primary reason for the bottleneck is the lack of transmission,” Bill Gates wrote in a recent blog post about transmission lines.

The stakes are high.

Herding cats with competing interests

Building new transmission lines requires countless stakeholders to come together and hash out a compromise about where a line will run and who will pay for it.

There are 3,150 utility companies in the country, the U.S. Energy Information Administration told CNBC, and for transmission lines to be constructed, each of the affected utilities, their respective regulators, and the landowners who will host a line have to agree where the line will go and how to pay for it, according to their own respective rules.

Aubrey Johnson, a vice president of system planning for the Midcontinent Independent System Operator (MISO), one of seven regional planning agencies in the U.S., compared his work to making a patchwork quilt from pieces of cloth.

“We are patching and connecting all these different pieces, all of these different utilities, all of these different load-serving entities, and really trying to look at what works best for the greatest good and trying to figure out how to resolve the most issues for the most amount of people,” Johnson told CNBC.

What’s more, the parties at the negotiating table can have competing interests. For example, an environmental group is likely to disagree with stakeholders who advocate for more power generation from a fossil-fuel-based source. And a transmission-first or transmission-only company involved is going to benefit more than a company whose main business is power generation, potentially putting the parties at odds with each other.

The system really flounders when a line would span a long distance, running across multiple states.

States “look at each other and say: ‘Well, you pay for it. No, you pay for it.’ So, that’s kind of where we get stuck most of the time,” Rob Gramlich, the founder of transmission policy group Grid Strategies, told CNBC.

“The industry grew up as hundreds of utilities serving small geographic areas,” Gramlich told CNBC. “The regulatory structure was not set up for lines that cross 10 or more utility service territories. It’s like we have municipal governments trying to fund an interstate highway.”

This type of headache and bureaucratic consternation often prevent utilities or other energy organizations from even proposing new lines.

“More often than not, there’s just not anybody proposing the line. And nobody planned it. Because energy companies know that there’s not a functioning way really to recover the costs,” Gramlich told CNBC.

Electrical transmission towers during a heatwave in Vallejo, California, US, on Sunday, Sept. 4, 2022. Blisteringly hot temperatures and a rash of wildfires are posing a twin threat to California’s power grid as a heat wave smothering the region peaks in the days ahead. Photographer: David Paul Morris/Bloomberg via Getty Images

Who benefits, who pays?

Energy companies that build new transmission lines need to get a return on their investment, explains James McCalley, an electrical engineering professor at Iowa State University. “They have got to get paid for what they just did, in some way, otherwise it doesn’t make sense for them to do it.”

Ultimately, an energy organization — a utility, cooperative, or transmission-only company — will pass the cost of a new transmission line on to the electricity customers who benefit.

“One principle that has been imposed on most of the cost allocation mechanisms for transmission has been, to the extent that we can identify beneficiaries, beneficiaries pay,” McCalley said. “Someone that benefits from a more frequent transmission line will pay more than someone who benefits less from a transmission line.”

But the mechanisms for recovering those costs varies regionally and on the relative size of the transmission line.

Regional transmission organizations, like MISO, can oversee the process in certain cases but often get bogged down in internal debates. “They have oddly shaped footprints and they have trouble reaching decisions internally over who should pay and who benefits,” said Gramlich.

The longer the line, the more problematic the planning becomes. “Sometimes its three, five, 10 or more utility territories that are crossed by needed long-distance high-capacity lines. We don’t have a well-functioning system to determine who benefits and assign costs,” Gramlich told CNBC. (Here is a map showing the region-by-region planning entities.)

Johnson from MISO says there’s been some incremental improvement in getting new lines approved. Currently, the regional organization has approved a $10.3 billion plan to build 18 new transmission projects. Those projects should take seven to nine years instead of the 10 to 12 that is historically required, Johnson told CNBC.

“Everybody’s becoming more cognizant of permitting and the impact of permitting and how to do that and more efficiently,” he said.

There’s also been some incremental federal action on transmission lines. There was about $5 billion for transmission-line construction in the IRA, but that’s not nearly enough, said Gramlich, who called that sum “kind of peanuts.”

The U.S. Department of Energy has a “Building a Better Grid” initiative that was included in President Joe Biden’s Bipartisan Infrastructure Law and is intended to promote collaboration and investment in the nation’s grid.

In April, the Federal Energy Regulatory Commission issued a notice of proposed new rule, named RM21-17, which aims to address transmission-planning and cost-allocation problems. The rule, if it gets passed, is “potentially very strong,” Gramlich told CNBC, because it would force every transmission-owning utility to engage in regional planning. That is if there aren’t too many loopholes that utilities could use to undermine the spirit of the rule.

What success looks like

Gramlich does point to a couple of transmission success stories: The Ten West Link, a new 500-kilovolt high-voltage transmission line that will connect Southern California with solar-rich central Arizona, and the $10.3 billion Long Range Transmission Planning project that involves 18 projects running throughout the MISO Midwestern region.

“Those are, unfortunately, more the exception than the rule, but they are good examples of what we need to do everywhere,” Gramlich told CNBC.

This map shows the 18 transmission projects that make up the $10.3 billion Long Range Transmission Planning project approved by MISO. Map courtesy MISO

In Minnesota, the nonprofit electricity cooperative Great River Energy is charged with making sure 1.3 million people have reliable access to energy now and in the future, according to vice president and chief transmission officer Priti Patel.

“We know that there’s an energy transition happening in Minnesota,” Patel told CNBC. In the last five years, two of the region’s largest coal plants have been sold or retired and the region is getting more of its energy from wind than ever before, Patel said.

Great River Energy serves some of the poorest counties in the state, so keeping energy costs low is a primary objective.

“For our members, their north star is reliability and affordability,” Patel told CNBC.

An representative of the Northland Reliability Project, which Minnesota Power and Great River Energy are working together to build, is speaking with community members at an open house about the project and why it is important. transmission lines, energy grid, clean energy

Great River Energy and Minnesota Power are in the early stages of building a 150-mile, 345 kilovolt transmission line from northern to central Minnesota. It’s called the Northland Reliability Project and will cost an estimated $970 million.

It’s one of the segments of the $10.3 billion investment that MISO approved in July, all of which are slated to be in service before 2030. Getting to that plan involved more than 200 meetings, according to MISO.

The benefit of the project is expected to yield at least 2.6 and as much as 3.8 times the project costs, or a delivered value between $23 billion and $52 billion. Those benefits are calculated over a 20-to-40-year time period and take into account a number of construction inputs including avoided capital cost allocations, fuel savings, decarbonization and risk reduction.

The cost will eventually be borne by energy users living in the MISO Midwest subregion based on usage utility’s retail rate arrangement with their respective state regulator. MISO estimates that consumers in its footprint will pay an average of just over $2 per megawatt hour of energy delivered for 20 years.

But there is still a long process ahead. Once a project is approved by the regional planning authority — in this case MISO — and the two endpoints for the transmission project are decided, then Great River Energy and Minnesota Power are responsible for obtaining all of the land use permits necessary to build the line.

“MISO is not going to be able to know for certain what Minnesota communities are going to want or not want,” Patel told CNBC. “And that gives the electric cooperative the opportunity to have some flexibility in the route between those two endpoints.”

For Great River Energy and Minnesota Power, a critical component of engaging with the local community is hosting open houses where members of the public who live along the proposed route meet with project leaders to ask questions.

For this project, the utilities specifically planned the route of the transmission to run along a previously existing corridors as much as possible to minimize landowner disputes. But it’s always a delicate subject.

A map of the Northland Reliability Project, which is one of 18 regional transmission projects approved by MISO, the regional regulation agency. It’s estimated to cost $970 million. Map courtesy Great River Energy

“Going through communities with transmission, landowner property is something that is very sensitive,” Patel told CNBC. “We want to make sure we understand what the challenges may be, and that we have direct one-on-one communications so that we can avert any problems in the future.”

At times, landowners give an absolute “no.” In others, money talks: the Great River Energy cooperative can pay a landowner whose property the line is going through a one-time “easement payment,” which will vary based on the land involved.

“A lot of times, we’re able to successfully — at least in the past — successfully get through landowner property,” Patel said. And that’s due to the work of the Great River Energy employees in the permitting, siting and land rights department.

“We have individuals that are very familiar with our service territory, with our communities, with local governmental units, and state governmental units and agencies and work collaboratively to solve problems when we have to site our infrastructure.”

Engaging with all members of the community is a necessary part of any successful transmission line build-out, Patel and Johnson stressed.

At the end of January, MISO held a three-hour workshop to kick off the planning for its next tranche of transmission investments.

“There were 377 people in the workshop for the better part of three hours,” MISO’s Johnson told CNBC. Environmental groups, industry groups, and government representatives from all levels showed up and MISO energy planners worked to try to balance competing demands.

″And it’s our challenge to hear all of their voices, and to ultimately try to figure out how to make it all come together,” Johnson said.

By: Catherine Clifford View the original article here

Heavy electrical transmission lines at the powerful Ivanpah Solar Electric Generating System, located in California’s Mojave Desert at the base of Clark Mountain and just south of this stateline community on Interstate 15, are viewed on July 15, 2022 near Primm, Nevada. The Ivanpah system consists of three solar thermal power plants and 173,500 heliostats (mirrors) on 3,500 acres and features a gross capacity of 392 megawatts (MW). George Rose | Getty Images News | Getty Images

Wind and solar power generators wait in yearslong bureaucratic lines to connect to the power grid, only to be faced with fees they can’t afford, forcing them to scramble for more money or pull out of projects completely.

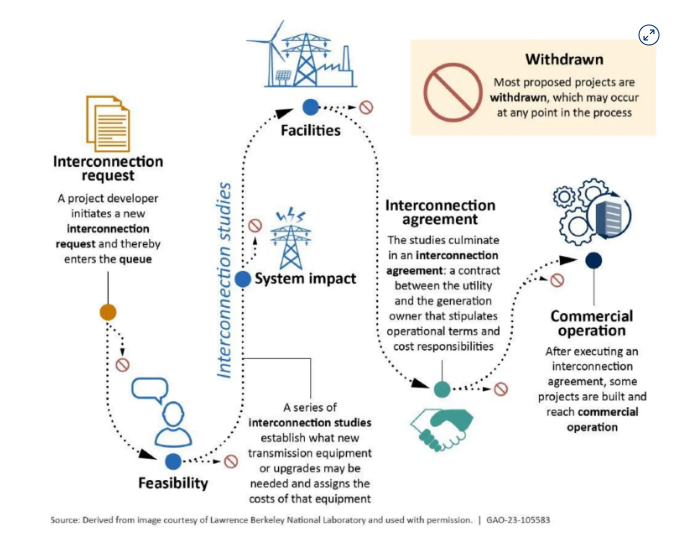

This application process, called the interconnection queue, is delaying the distribution of clean power and hampering the U.S. in reaching its climate goals.

The interconnection queue backlog is a symptom of a larger climate problem for the United States: There are not enough transmission lines to support the transition from a fossil fuel-based electric system to a decarbonized energy grid.

Surprise fee increases

The Oceti Sakowin Power Authority, a nonprofit governmental entity owned by seven Sioux Indian tribes, is working to build 570 megawatts of wind power generation to sell to customers in South Dakota.

“Economic development through renewable energy speaks to the very heart of Lakota culture and values – being responsible stewards of Grandmother Earth, Unci Maka,” Jonathan E. Canis, general counsel for the Oceti Sakowin Power Authority, told CNBC. “Together our tribes occupy almost 20% of the land area of South Dakota. And the experts who have been measuring our wind resources literally describe them as ‘screamin.’.”

To connect wind power generation to the electric grid and make money from the sale of that power, the Oceti Sakowin Power Authority — like every electricity generator in the U.S. — has to submit an application called an interconnection request to whichever organization is overseeing the coordination of the electric grid in that region. Sometimes it’s a regional transmission planning authority, other times a utility.

This photo shows the rangeland on the Cheyenne River Reservation with the Missouri River in the distance. The Oceti Sakowin Power Authority wants to build two wind power projects and the Ta’teh Topah project, planned to be 450 megawatts, is the larger of two wind projects. The transmission tie-line for the Ta’teh Topah project will cross the rangeland and the river to interconnect with a Basin Electric transmission line east of the Missouri River. Photo courtesy Oceti Sakowin Power Authority.

In late 2017, the Oceti Sakowin Power Authority paid a $2.5 million deposit to secure a place in line for its application to be reviewed by the Southwest Power Pool, a regional grid operator.

Five years later, in 2022, the Southwest Power Pool came back and told it that the fee to connect to the grid would actually be $48 million. That’s because connecting all that new power to the grid would require major updates to the transmission infrastructure.

The Oceti Sakowin Power Authority had 15 business days to come up with the extra $45.5 million.

“Needless to say, we couldn’t do it and had to drop out,” Canis told CNBC.

Now, the Oceti Sakowin Power Authority is reevaluating the size and composition of the project and plans to reenter the interconnection queue by the end of the year. That could mean another yearslong wait in line.

These burdens are typical.

In 2020, Pine Gate Renewables had a solar project located in the Piedmont region of North Carolina that it expected to cost $5 million to connect to the electric grid. The local utility in charge of overseeing the interconnection process told Pine Gate it would be more than $30 million. Pine Gate had to terminate the project because it couldn’t afford the new fees, its vice president of regulatory affairs, Brett White, told CNBC.

“We view, as a company, the interconnection problem as the biggest impediment to the industry right now and the costs associated with interconnection are the biggest reason that a project dies on the vine,” White said. “It’s the biggest wild card you have going into the project development cycle.”

There are efforts underway to improve the efficiency of the process, but they’re fundamentally putting a Band-Aid on top of an even deeper problem in the United States: There isn’t enough transmission infrastructure to support the energy transition from fossil fuel sources of energy to clean sources of energy.

“You could make the process for the queue as efficient and pristine as possible and it still could not be all that effective because at some point you’re going to run out of transmission headroom,” Wood Mackenzie analyst Ryan Sweezey told CNBC.

This photo shows the Western Area Power Administration’s substation in Martin South Dakota on the Pine Ridge Reservation where the 120 megawatt Pass Creek project, the smaller of the two wind power projects Oceti Sakowin Power Authority is trying to stand up, will interconnect if the project can move forward. Photo courtesy Oceti Sakowin Power Authority.

Waiting in line

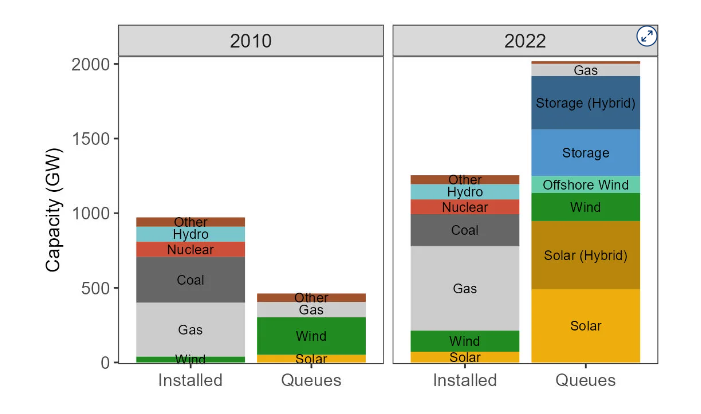

The entire electric grid in the U.S. has installed capacity of 1,250 gigawatts. There are currently 2,020 gigawatts of capacity in the interconnection queue lines around the country, according to a report published Thursday by the Lawrence Berkeley National Laboratory. That includes 1,350 gigawatts of power capacity, mostly clean, looking to be constructed and connected to the grid. The rest, 670 gigawatts, is for storage.

In 2022, the active energy capacity in interconnection queues in the U.S. is about 2,020 gigawatts and exceeds the installed capacity of entire U.S. power plant fleet, which is about 1,250 gigawatts, according to the report on interconnection queues out of Lawrence Berkeley National Laboratory published Thursday. Chart courtesy Joseph Rand at Lawrence Berkeley National Laboratory.

Berkeley Lab pulls interconnection queue data from all of the regional planning territories in the United States and from between 35 and 40 utilities that are not covered by areas with regional planning authorities. The data covers between 85% and 90% of the electricity load in the United States, Joseph Rand, an energy policy researcher and the lead author of the study, told CNBC.

The interconnection process starts with a request to connect to the grid, which officially enters the power generator in the interconnection queue. The next step is a series of studies — the feasibility, system and facilities studies — where the grid operator determines what equipment or upgrades will be necessary to get the new power generation on the grid and what it will cost.

If all the parties can agree, then the power generator and grid operator reach an interconnection agreement, which establishes the grid improvements the power generator will pay for.

The total power capacity that comes out from a fossil fuel-burning power plant is often much greater than the capacity from renewable plants. That means it can take multiple wind or solar power generation plants — and, therefore, interconnection requests — to get the same units of energy online.

A single natural gas plant could be 1,200 megawatts, Sweezey told CNBC. “That’s one request — 1,200 megawatts,” Sweezey said. “Whereas usually if you’re going to get that same amount of capacity with renewables, that’s going to be six, seven, eight, nine, 10 different projects. So that’s 10 different requests in the queue.”

On average, it took a new power generation project 35 months to go from the interconnection request being filed with a grid operator to an interconnection agreement being reached in 2022, according to Berkeley Lab.

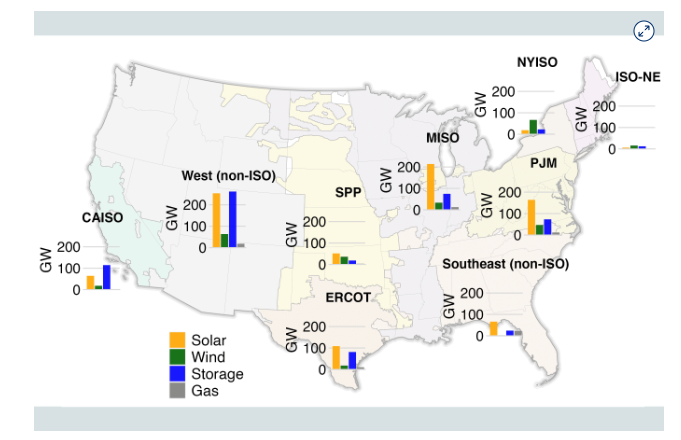

The amount of electricity generation in queues by region by type of power, according to the report on interconnection queues out of Lawrence Berkeley National Laboratory published Thursday. Chart courtesy Joseph Rand at Lawrence Berkeley National Laboratory.

How did this process become such a problem?

The U.S. energy grid is a patchwork system of many regional utility companies. Some provide transmission services and some don’t.

In an effort to promote competition, the Federal Energy Regulatory Commission issued an order in 1996 saying transmission service has to be provided to power generators on a nondiscriminatory basis. This allowed all kinds of power generators, including those that do not own transmission infrastructure, to compete. In 2003, it issued another order that standardized the interconnection process for energy generators.

Both orders “attempted to make the services one needs nondiscriminatory and fair to all users, for their respective service,” according to Rob Gramlich, founder of transmission market intelligence firm Grid Strategies.

This is a simplified visualization of the interconnection queue study process. Chart courtesy the Government Accountability Office and Lawrence Berkeley National Laboratory.

That process worked well enough when the power generation industry was building large, centrally located energy plants that burned fossil fuels. But the process started to show signs of strain around 2008 when renewable energy started to come online in places where there was not sufficient transmission, Gramlich told CNBC. In April 2008, MISO, one of the regional operators, said it would take 42 years, until 2050, for it to get through its interconnection queue.

Reforms in 2008 and 2012 helped a little bit, Gramlich told CNBC. “But I think everybody’s realizing now that that original process is fundamentally unsuited to the new generation mix.”

The interconnection process is especially bad at estimating battery storage, said White. That’s because transmission planning is always defaulting to the worst-case scenario, but batteries will draw energy from the grid when the demand is low and energy prices are low, and then use that stored power when the grid is at or near capacity. Using worst-case-scenario planning for battery storage fundamentally misses the point of a battery.

“The upgrades that are going to be triggered on the system are going to be very, very extensive and very, very expensive. And so they hand you a bill that reflects that,” White told CNBC.

But that kind of system upgrade “in our mind is totally disassociated from the economics of the asset, and not really looking at the benefit that the project is going to provide to the system,” White said.

Texas makes it easier

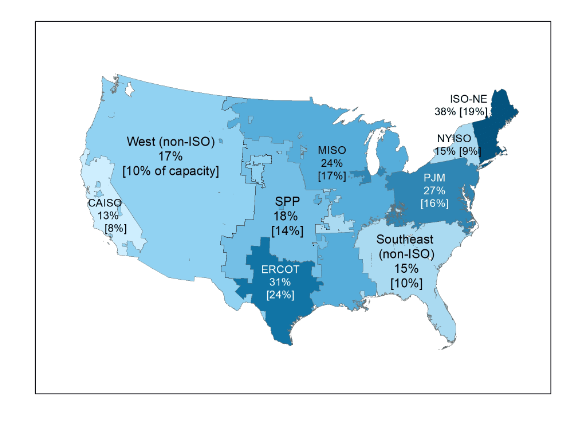

The rates of interconnection applications that actually reach commercial completion vary significantly, but none are higher than 38% in the New England region, according to Berkeley Lab. The Texas grid operator, Electric Reliability Council of Texas, or ERCOT, has a completion rate of 31% and is the only other region with a completion rate of over 30%.

On the low end, the California Independent System Operator region has an 13% completion rate and the New York Independent System Operator region is at 15%.

This chart shows the share of projects that requested interconnection from 2000 to 2017 that have reached a commercial operation date. Chart courtesy Joseph Rand at Lawrence Berkeley National Laboratory.

The low percentage of interconnection requests that actually get built is partly because of the high cost to connect.

In the MISO region, for instance, interconnection costs were generally less than $100 per kilowatt-hour from 2008 to 2016, but have risen to a few hundred dollars per kWh for wind and solar, with spikes as high as $1,000 per kWh in some parts of the region, Gramlich told CNBC.

Adding even small amounts of energy to the grid requires infrastructure improvements because it’s nearly at capacity. Pushing those costs onto the builders of individual renewable projects generally makes them economically unsustainable.

“Those projects ended up withdrawing from the queue or terminating, because they don’t pencil anymore,” White told CNBC.

Some of the completion rates are artificially low because developers don’t actually expect to complete them all, but instead shop the same project around to various regional grid operators to get the best deal — what’s called “speculative queuing,” Sweezey told CNBC. It’s not expensive to get into queues, so developers submit applications to get information about which location will require the least expensive upgrades.

For grid operators, having power generators stuff their queues is overwhelming an already taxed system.

“Projects that have come through the process are not being built and becoming operational,” Jeffrey Shields, a PJM Interconnection spokesperson, told CNBC. “There are about 38,000 MW of renewable projects that have no further PJM requirements but are not being built because of siting, supply chain, or other issues facing the industry that are not related to PJM’s interconnection process.”

The long application timelines and expensive upgrades have made Texas a desirable place to build renewable energy projects because the state has its own interconnection application process.

“There is Texas, and then there’s the rest of the country with respects to interconnection,” White of Pine Gate told CNBC. Texas doesn’t require the same level of network upgrades to get power generation connected to the grid so getting a project online in Texas is faster and lower cost than the rest of the country, White said.

“You can put a project in the PJM queue tomorrow and it may not get constructed and built until 2030, whereas if you do the same with the Texas project, right now, it’s probably online in two to three years. So it’s just a much, much shorter timeline to commercial operation for a project in Texas,” White told CNBC.

But Texas also has a unique risk because ERCOT can decide to limit the amount of power that a generator can sell to the market if a particular electric corridor gets overly congested.

“It’s a bit of a double-edged sword,” White told CNBC. But with infrastructure deals, “time kills deals, time kills projects,” White said, so energy developers may prefer to take the risk and get the deal done.

Huge clouds and transmission towers are seen from Highway 5 in Kern County of California, United States on April 2, 2023. Anadolu Agency | Anadolu Agency | Getty Images

How does this situation get fixed?

In June 2022, FERC issued a proposal on interconnection reforms to address queue backlogs and has since received a slew of public comments.

“We understand that 80 to 85 percent of the projects that are waiting in the queue ultimately are not being built. I think FERC has an opportunity here to make sure that we unlock that bottleneck and that we do all that we can to move those projects forward,” FERC Chairman Willie Phillips said on March 16, according to a statement provided by a FERC spokesperson.

The proposed rule change would offer incremental improvements, like providing information to developers so they can make more informed siting decisions without flooding the queue with speculative requests, and imposing more strict mandates on the regional grid operators to complete studies in a given time period, Rand of Berkeley Lab told CNBC.

“I do think what FERC is proposing has the potential to improve this situation,” Rand told CNBC. But fundamentally, these iterative changes won’t be a silver bullet.

“The energy transition is here. But our updating and expansion of our electric transmission system so far has not even remotely kept pace with that velocity, rate of change we are seeing on the generator-supply side,” said Rand.

There’s also a shortage of the kinds of electrical and transmission engineers required to process all of these applications, Sweezey and White told CNBC. “There’s just not enough people and so we have to think about what is the smartest way to maximize that expertise. And that means getting those engineers out of some of the rote manual data entry and into the actual analysis,” White told CNBC.

Another option is building new sources of clean energy that can be constructed closer to where demand is needed, like small nuclear reactors, Sweezey told CNBC. “I just don’t think people have come to that realization yet.”

Building sufficient transmission to support the energy transition is not necessarily a technical challenge as much as it is a political one.

“The type of coordination and planning that’s required for this kind of large-scale transmission — this involves maybe multiple utilities, multiple grid operators, multiple states, cities, counties, everything, even the feds are all involved — and that is antithetical to the U.S. as structured as a decentralized nation,” Sweezey told CNBC.

But the stakes are high.

“Even with all of the work, with all this great stuff that’s in the IRA and all of the wind that is in the sails of decarbonization in the renewable industry, if you can’t address transmission and infrastructure, then those goals aren’t going to be met,” White told CNBC.

“It really is the bottleneck that’s preventing that from happening.”

Regulators and policymakers must resist the temptation to overcommit to hydrogen for end uses where electrification will ultimately win out.

By: Dan Esposito and Hadley Tallackson View the original article here

This opinion piece is part of a series from Energy Innovation’s policy experts on advancing an affordable, resilient and clean energy system. It was written by Dan Esposito, senior policy analyst in Energy Innovation’s Electricity Program, and Hadley Tallackson, a policy analyst in the Electrification Program at Energy Innovation.

The Inflation Reduction Act has upended hydrogen economics, making “green” hydrogen — electrolyzed from renewable electricity and water — suddenly cost-competitive with its natural gas-derived counterpart.

On the supply side, electrolyzers can help utilities integrate renewables into the grid, speeding the clean electricity transition. On the demand side, electrolysis can cost-effectively decarbonize hydrogen production.

But the new hydrogen economics mean regulators and policymakers must be even more careful to avoid directing the fuel to counterproductive applications like heating buildings.

“Gray” hydrogen, which uses the highly-polluting steam methane reformation, or SMR, process, has long been the cheapest production method, trading around $1.50-2.00 per kilogram in the United States. In comparison, electrolyzed hydrogen costs about $4-8/kg without subsidies. The Inflation Reduction Act’s $3/kg incentive for zero-carbon hydrogen makes green hydrogen cheaper than gray, potentially spurring an electrolyzer boom.

To facilitate utilities connecting newly-cheap electrolyzers to the grid, regulators should set tariffs reflecting their flexibility value, empowering more bullish utility wind and solar resource procurement.

However, cheap hydrogen should not encourage its use in applications better served by direct electrification like buildings or transportation. Regulators should remain wary of gas utility proposals to blend hydrogen into pipelines, as they would achieve few emissions reductions before facing costly dead-ends while increasing threats to public safety. State policymakers should also use caution before directing public funds toward hydrogen light-duty refueling stations, as electric vehicles have substantial cost and performance advantages that risk stranding hydrogen vehicle infrastructure.

Instead, industrial consumers should use green hydrogen to decarbonize their gray hydrogen consumption for a cheaper, cleaner product.

The IRA’s clean hydrogen production tax credits

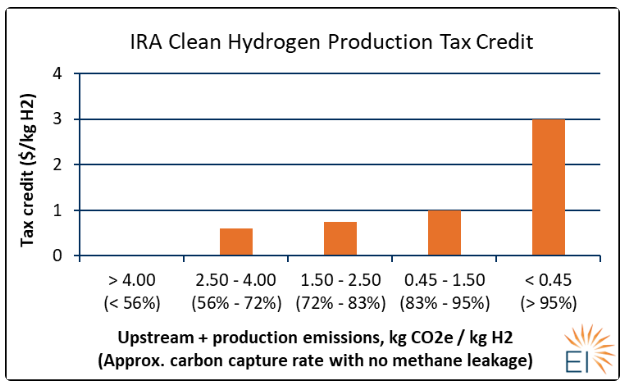

The Inflation Reduction Act offers a 10-year production tax credit for “clean hydrogen” production facilities. Incentives begin at $0.60/kg for hydrogen produced in a manner that captures slightly more than half of SMR process carbon emissions, assuming workforce development and wage requirements are met. The PTC’s value rises to $1.00/kg with higher carbon capture rates before jumping to $3.00/kg for hydrogen produced with nearly no emissions.

The carbon capture rate estimates assume an emissions rate of 9.00 kg CO2e / kg H2 from producing gray hydrogen. Permission granted by Energy Innovation Policy and Technology.

However, the IRA’s “clean hydrogen” definition includes upstream emissions, including methane leakage from natural gas pipelines. Since methane is a much more potent greenhouse gas than carbon dioxide, even small leaks significantly increase the carbon capture rate needed to qualify for different PTC tiers.

This suggests “blue” hydrogen produced from pairing SMR and carbon capture and sequestration technology won’t qualify for the highest PTC value. Even hydrogen produced via pyrolysis — which uses natural gas but has no process emissions — may be knocked into lower tiers with enough methane leakage.

Green hydrogen therefore has a $3/kg subsidy advantage over gray and at least a $2/kg advantage over blue. These subsidies will be lower in practice, as the 10-year PTC will be spread over the facilities’ 15-or-more year lifetimes, but they still shift the hydrogen economics paradigm.

The opportunity: Cleaning today’s gray hydrogen while boosting renewable integration

The Inflation Reduction Act makes clean hydrogen production very cheap, but hydrogen faces costs for transportation, storage and conversion to other compounds. The U.S. also lacks hydrogen-compatible pipelines, storage caverns, refueling stations, and equipment like consumer appliances.

The first best use for clean hydrogen is circumventing these mid- and downstream cost and infrastructure challenges. Namely, clean hydrogen can plug-and-play to replace today’s gray hydrogen production.

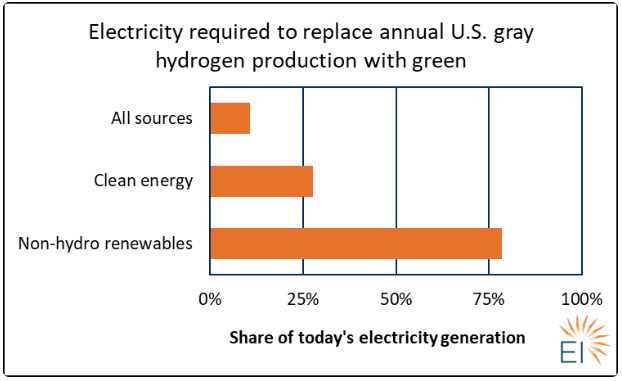

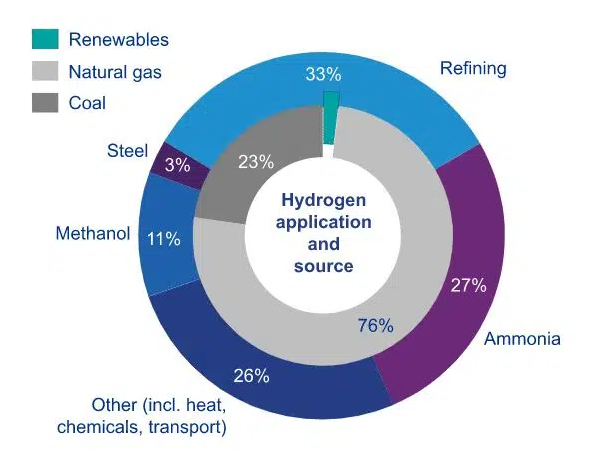

For example, ammonia facilities and oil refineries use 90% of U.S. annual hydrogen production. Electrolyzers sited nearby can opportunistically produce clean hydrogen to reduce facilities’ fuel costs and emissions.

The gray hydrogen replacement market is huge — 90% of 2021 U.S. utility-scale wind and solar electricity would be required to produce it all via electrolysis. Green hydrogen also has a 25% to 50% greater GHG emissions reduction impact when replacing gray hydrogen than natural gas.

Non-hydro renewables includes wind, solar, biomass, and geothermal. Data excludes distributed generation. Permission granted by Energy Innovation Policy and Technology.

This process can speed renewable energy deployment. Grid-connected electrolyzers can draw from renewables when electricity is cheap, helping finance them for power that would otherwise fetch low prices or be curtailed. When electricity prices rise, electrolyzers can ramp down, allowing the renewables to meet demand and keeping hydrogen production cheap.

The combination is a win-win: grid-connected, price-responsive electrolyzers help clean the industrial sector and power grid without committing to extensive new hydrogen-ready infrastructure and appliances. As U.S. renewables deployment accelerates, the demand for complementary green hydrogen may grow apace, including feeding an enormous clean ammonia export market.

The risk: Misallocating public funds for myopic projects

The Inflation Reduction Act’s clean hydrogen PTC is a massive incentive and can make many potential hydrogen end-uses look attractive. However, these propositions are often a mirage.

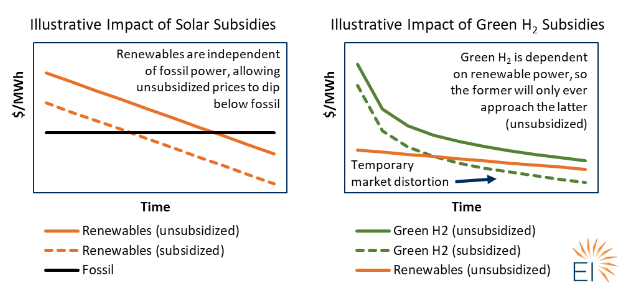

Clean hydrogen tax credits will reduce electrolyzer capital costs, helping unsubsidized green hydrogen production costs converge toward the cost of renewable electricity. However, since renewable electricity will always be an input to electrolysis, unsubsidized green hydrogen will never be cheaper than direct use of renewable electricity, even though the $3/kg credit is large enough to temporarily distort the market in hydrogen’s favor. By contrast, renewable energy subsidies are helping unsubsidized wind and solar become cheaper than fossil fuel power plants, as these resources’ costs are independent of each other.

Rightmost chart assumes green hydrogen is used for electricity production ($/MWh), but metaphor extends to any use-case where electricity and hydrogen can compete on the same time-scale. Permission granted by Energy Innovation Policy and Technology.

Despite these dynamics, suddenly cheap hydrogen will amplify the fuel’s hype, inviting proposals for investing in hydrogen infrastructure and compatible end-use equipment. Such actions risk wasting time and money on research or infrastructure that will be underutilized or stranded once Inflation Reduction Act subsidies expire.

For example, gas utility plans to blend hydrogen with natural gas may be cost-effective with the subsidies, but they heighten safety and public health risks and aren’t long-term decarbonization strategies. By comparison, electric appliances like heat pumps and induction stoves use clean electricity approximately four times more efficiently than green hydrogen equivalents.

Other proposals may entail committing public funds to sprawling new infrastructure networks including pipelines and refueling stations to support hydrogen-powered fuel cell vehicles. Yet electric light-duty vehicles hold clear, insurmountable advantages that may be veiled by heavily subsidized hydrogen.

Hydrogen infrastructure proposals will sometimes be worthwhile. For example, geologic caverns for seasonal electricity storage can help clean the last 10% to 20% of the power grid, using green hydrogen to generate electricity when renewables and batteries are unavailable. Hydrogen can also be used as a feedstock or fuel for high-heat industrial processes. But in these cases, hydrogen’s advantage comes from filling a niche that direct electrification cannot, making its inefficiencies irrelevant.

Setting up for success

The IRA’s clean hydrogen tax credits can accelerate a reliable clean electricity transition while beginning to decarbonize industry — if applied judiciously.

Supporting a clean power grid will require incentivizing developers to connect electrolyzers to the grid rather than build standalone projects with co-located renewables, as only the former will allow utilities to benefit from electrolyzers’ flexible demand.

The U.S. Treasury should issue guidance clarifying how electrolytic hydrogen’s carbon intensity will be measured. Its framework should explicitly permit electrolyzers to connect to the grid, using collocated renewables, power purchase agreements, or potentially renewable energy credits to confirm they’re powered by renewables.

Regulators should direct electric utilities to set electrolyzer-specific tariffs, as current industrial tariffs may be mismatched with the flexibility value electrolyzers provide. They should also ease interconnection constraints and build more transmission, both of which can connect co-located renewables and electrolyzer projects to the grid. More grid-connected electrolyzers should then give regulators greater confidence to fast-track utilities’ renewable deployment schedules.

Industry consumers should explore contracts that allow clean hydrogen to replace some or all of their gray hydrogen, reducing costs and providing a cleaner product that may fetch higher prices from climate-conscious purchasers.

However, regulators and policymakers should steel their resolve against temptations to overcommit to hydrogen for end-uses where electrification will ultimately win out.

Research and development should focus on ways clean hydrogen can decarbonize hard-to-electrify sectors like aviation and shipping and boost long-duration electricity storage, rather than focusing on blending hydrogen into natural gas pipelines, using hydrogen for low-heat industrial processes, or designing hydrogen-capable consumer appliances. Limited state funds for commercialization should support electric infrastructure like electric vehicle charging stations and heat pumps, letting private companies take the risk for ventures like hydrogen refueling stations.

Together, these strategies can ensure the Inflation Reduction Act clean hydrogen tax credits maximize their value in reducing GHG emissions without inadvertently leading states and utilities down futile paths.

The signing of the U.S. Inflation Reduction Act (IRA) — enacted into law on Aug. 16, 2022 — heralds significant and long-term changes for renewable energy development and energy storage installations. The new law represents the single largest climate-related investment by the U.S. government to date, allocating $369 billion (USD) for energy and climate initiatives to help transition the U.S. economy toward more sustainable energy resources.

According to industry estimates, the IRA stands to more than triple U.S. clean energy production, which would result in about 40% of the country’s energy coming from renewable sources such as wind, solar and energy storage by 2030. This would mean an additional 550 gigawatts of electricity generated via renewable sources in less than 10 years.

The IRA’s expected impacts present significant opportunities for renewable energy developers and energy storage companies. Below, we discuss the law’s key effects on the renewable and storage industries, with a special focus on critical technology, software and advisory support for companies launching or expanding their renewable energy projects as the new law takes effect.

More reliable tax credit structures likely to transform renewable energy development

Crucially, the IRA establishes long-term energy tax credit structures to support renewable energy development, giving companies a more stable 10-year window for such incentives versus the previous on-again, off-again incentives that drove “boom and bust” cycles of renewables projects.

Renewables industry trade group American Clean Power reports that for the second quarter of 2022, more than 32 gigawatts of renewable energy projects were delayed, and new project development and installations also fell to their lowest levels since 2019. The group attributes these slumping performance statistics to uncertainty in tax and incentive policies along with transmission challenges and trade restrictions; provisions of the IRA may help reverse this performance trajectory.

“Historically, the U.S. renewables industry has relied on tax credits that required reauthorization from Congress every few years, which created boom-bust cycles and significant challenges in terms of planning for long-term growth,” explained Gillian Howard, global director of sustainable energy and infrastructure at UL Solutions. She added that the IRA establishes a 10-year policy in terms of tax credits for wind, solar and energy storage projects. The new law also provides incentives for green hydrogen, carbon capture, U.S. domestic energy manufacturing and transmission, Howard noted.

“We expect the IRA to both significantly accelerate and increase the deployment of new renewable energy projects in the U.S. over the next decade,” Howard says. “This will be transformational.”

Standalone storage now eligible for tax credits: a long-awaited change and major IRA impact

The use of energy storage has taken on added urgency in recent years as extreme weather and geopolitical issues increasingly challenge energy access and reliability. Projects for energy storage, including batteries and thermal and mechanical storage, have previously been included in investment tax credit programs. Now the IRA extends tax credits for energy storage through 2032. The new law also opens tax credit eligibility to standalone energy storage, which entails storage units constructed and operated independently of larger energy grids.

“Providing an investment tax credit for standalone storage is the single-most important policy change in the IRA — period,” said David Mintzer, energy storage director at UL Solutions. “This one change sets up all of the other energy storage advantages gained from the new law. Those of us in the BESS industry have been waiting for this to happen for more than 10 years, and this is the most significant legislation to accelerate the transition to clean energy and smart grids.”

Mintzer noted that the IRA allows placement of battery energy storage systems (BESSs) where energy demand is highest and removes longstanding requirements that storage systems must be paired to solar sources. Accordingly, key impacts of the new law on energy storage projects in the U.S. will likely include the following near-term impacts:

Standalone utilities – The IRA provides more substantial economic incentives for more sites (nodes) that connect to grid networks in support of wholesale energy and additional dispatch services.

Standalone distributed generation – More flexible placement of standalone BESSs can support economic arguments for commercial development at sites with inadequate access to larger energy grids.

Storage technologies – The IRA’s tax credit provisions for standalone energy storage will prompt research and development and, ultimately, the execution of more and different types of batteries.

Banking – Smaller banks and lending organizations may be more likely to finance the construction and development of smaller energy storage systems versus larger and costlier main-grid projects.

“This decoupling of the storage-solar rules will enable BESS sites to be placed where they can provide the best economic returns,” Mintzer explained, adding that battery use will also become more flexible to better support energy grids. Ultimately, Mintzer said, developing and deploying more storage systems will help the U.S. achieve its clean energy goals.

Solar provisions: PTC versus ITC

The IRA includes provisions for 100% production tax credits (PTC) for solar, which transitions to a technology-neutral PTC in 2025. Until the passage of the IRA, solar developers could use the investment tax credit (ITC), which was originally set at 30% of eligible project costs, stepping down over the last few years to 26%, 22% and 0%. The IRA reset the ITC to 30% and provides an option for developers to opt for the PTC instead of the ITC. Rubin Sidhu, director of solar advisory services at UL Solutions, said, “Preliminary analysis shows that for projects with a high net capacity factor (NCF), PTC may be a more favorable option. Further, as solar equipment costs continue to decrease and NCFs continue to go up with better technology, PTC will be more favorable compared to ITC for more and more projects.”

Since the PTC is tied to actual energy generation by a project over 10 years, we expect the investors will be more sensitive to the accuracy of pre-construction solar resource and energy estimates, as well as the ongoing performance of projects.

Tools to support renewable energy development and storage in the IRA era

Launching renewable energy development and storage projects under the auspices of the IRA will require robust tools and technologies in order to manage these projects’ technical, operational and financial components in what may well become a more highly competitive and crowded field.

The degree to which a renewable energy developer will require third-party technologies and advisory partnerships will depend on the firm’s internal resources and commercial goals. Our experience at UL Solutions assessing more than 300 gigawatts worth of renewable energy projects has been that some firms require tools to evaluate and design projects themselves, while other companies seek full-project advisory support. To accommodate a diverse array of technology and advisory needs across the industry, UL Solutions has developed products and services, including:

Full energy and asset advisory services.

Due diligence support.

Testing and certification.

Software applications for solar, wind, offshore wind and energy storage projects.

Effective tools for early-stage feasibility and pre-construction assessments are crucial for the long-term viability of renewable energy development projects. UL Solutions provides modeling and optimizing tools for hybrid power projects via our Hybrid Optimization Model for Multiple Energy Resources (HOMER®) line of software, including HOMER Front for technical and economic analysis of utility-scale standalone and hybrid energy systems, HOMER Grid for cost reduction and risk management for grid-connected energy systems, and HOMER Pro for optimizing microgrid design in remote, standalone applications. UL Solutions also supports wind energy assessment projects with our Windnavigator platform for site prospecting and feasibility assessments, Windographer software for wind data analytics and visualization support, and Openwind wind farm modeling and layout design software.

For energy storage system developers, HOMER Front also features tools to design and evaluate battery augmentation plans as well as dispatch strategies, applicable when participating in merchant energy markets or contracting with power purchase agreements.

Conclusion: Reliable tools for a new frontier

Given the magnitude and scope of the IRA, it will take some time for regulatory implementation to play out. Effects of the new law will not be immediate. Over time, the IRA will provide more predictability and certainty in terms of tax credits and related incentives for renewable energy development and lays the groundwork for innovation and expansion of energy storage systems and technologies. Gaining a competitive advantage in this new era for renewables, nonetheless, will require the right software capabilities, third-party advisory support or both, depending on companies’ resources and commercial objectives.

The global energy market has become even more unstable and uncertain. Add to this the challenges caused by climate change. To meet future demand, sustainable and affordable energy supplies are a must, raising a question “is green hydrogen energy of the future?”

Recently, hydrogen is leading the debate on clean energy transitions. It has been present at industrial scale worldwide, offering a lot of uses but more so in powering things around us.

In the U.S., hydrogen is used by industry for refining petroleum, treating metals, making fertilizers, as well as processing foods.

Petroleum refineries use it to lower the sulfur content of fuels. NASA has also been using liquid hydrogen since the 1950s as a rocket fuel to explore outer space.

This warrants the question: is green hydrogen the energy of the future?

This article will answer the question by discussing hydrogen and its uses, ways of producing it, its different types, and how to make green hydrogen affordable.

Using Hydrogen to Power Things